Volvere - Where Patience is an Art Form

Volvere - Where Patience is an Art Form

If you want fireworks, you should certainly stay away from my top holding.

If you read yesterday’s article, you’ll know that Volvere (LON:VLE) is still my largest holding, and that it now stands at 24% of my share portfolio.

This is a company I first noticed all the way back in 2016, in a ShareProphets article that I titled “Volvere - A Great Investment Company at a Discount”.

Six years later, the company is still a great investment company (in my opinion), and it is again at a significant discount.

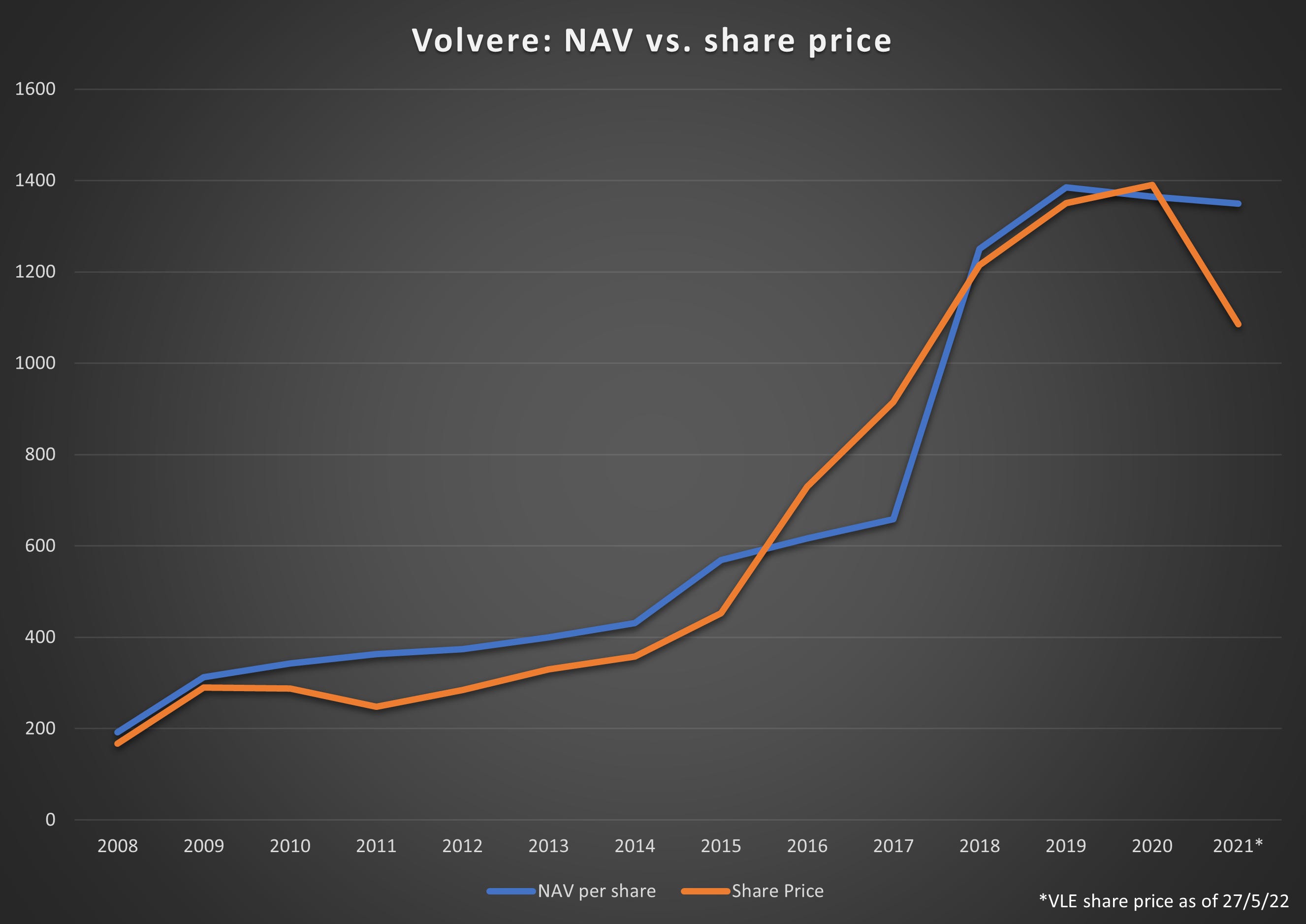

The investment vehicle managed by Jonathan and Nicholas Lander has a truly wonderful long-term track record. Let me show you in chart form the company’s net asset value per share.

I’ve also including the company’s share price recorded at the midpoint of the following year. For example, “2015” shows you the NAV at the end of 2015 (in blue), along with the share price in June 2016 (in red).

As you can see, Volvere’s share price has sometimes traded above the company’s last-reported annual NAV, but it more usually trades below this level.

Speaking of which, let’s take a look at the discount (or premium) in the share price each year. All calculations and errors are mine alone:

Prior to the results for December 2016, it was normal to find VLE trading at a discount of more than 15% to NAV.

After that, however, investors rightfully became excited about Volvere’s prospects, and the results of 2018 confirmed that the company’s NAV had been transformed by a £31 million disposal.

More recently however, news flow has been disappointingly quiet. Investors have once again become bored with the Volvere story, and the share price has sunk back to 1085p, an almost 20% discount to the NAV reported by the company earlier this week.

In other words, we are back to the sort of rating that the company received prior to its 2016 results.

In this article, I’m going to lay out for you my current view of the company’s prospects, and exactly what I intend to do with my Volvere shares.