An all-weather investment idea for stormy conditions

An all-weather investment idea for stormy conditions

CMC, IG Group and Coinbase: which of these can survive changing market conditions?

Macro concerns remain front and centre for many of us. I’m going to start this article with a look at today’s macro news, and then finish with a look at some investment ideas I like, regardless of the macro outlook.

An Historic Day in Monetary Policy

The ECB has today made a major announcement.

For years, the ECB has been propping up the EU financial system, keeping European government borrowing costs down and keeping asset prices high.

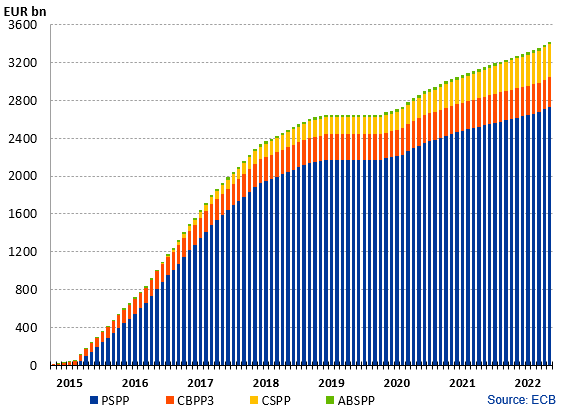

In total, its asset purchase programme has racked up €3.4 trillion of net purchases. The entire EU has a GDP of only around €14 trillion.

As a result of these policies at the ECB and other central banks, some of us have been predicting inflation for a long time (and investing accordingly).

Like stopped clocks, we have eventually been proven right, as inflation has now surged to a record high, far above the official target of 2%.

I now believe that almost anything the ECB does at this stage will be too little, too late. After what they’ve done to the M2 money supply, I think the outcome of this latest economic crisis is already baked into the cake (and banning Russian fossil fuels is only adding natural gas to the inflationary fire).

The announcement today is that there will be no further net asset purchases by the ECB, although their enormous €3.4 trillion portfolio won’t be reduced any time soon (reducing it would be truly deflationary!).

As for rates, we have a 25 basis point increase in July, and the promise of more hikes after that:

Looking further ahead, the Governing Council expects to raise the key ECB interest rates again in September. The calibration of this rate increase will depend on the updated medium-term inflation outlook…

Beyond September, based on its current assessment, the Governing Council anticipates that a gradual but sustained path of further increases in interest rates will be appropriate.

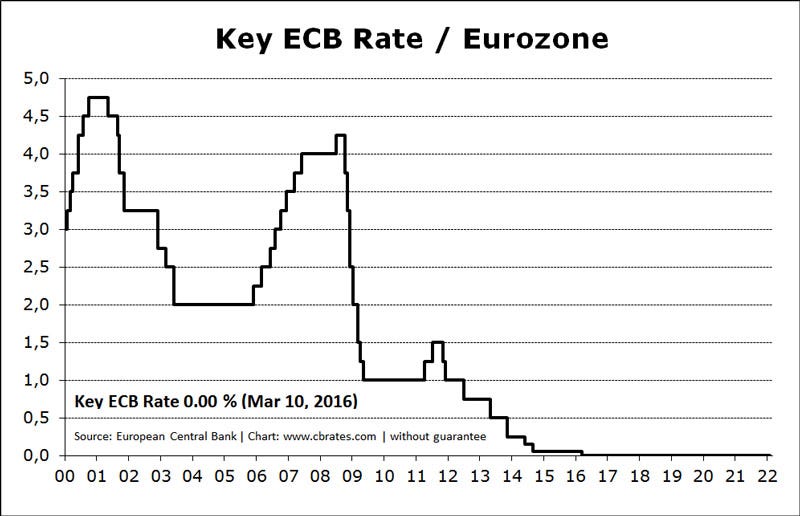

In monetary terms, this is a truly historic day, as we get the first uptick on this chart since 2016:

Asset Prices - Still too high

I’d invite you to look again at the above chart, and to bear in mind just how far we are from a “normal” rate of 4%, let alone from a rate that would be considered “high” by historical standards.

My career in the financial markets started around 2007. I saw Bernanke take over from Greenspan at the Fed, during an ill-fated attempt to raise rates whose primary effect was to burst the housing bubble.

As you can see, the European interest rate only made it to 4.25% before policymakers gave up and retreated lower. There have now been six long years of financial absurdity, also known as ZIRP (zero interest rate policy).

Many of those currently employed in finance have no memory at all of normal rates.

But without normal rates, the time value of money - i.e. the basis of valuing any financial asset - simply does not function as it should.

This explains the bewildering growth of pointless assets being treated as respectable investments, and absurd valuations which would make even the most gung-ho dot-com investor blush.

It explains the rise of investing gurus whose financial expertise, or lack thereof, would have been exposed in a previous era.

All of which brings me to a tweet this week from New York-based Galileo Russell, who made a name for himself as a Tesla bull on YouTube.

More recently, he has pivoted to other assets, and he wrote the below messages to his Twitter followers on Tuesday.

These messages translate as “I am willing to borrow from you at a silly interest rate if you’ll help me convert my speculative crypto assets into the overpriced shares of a crypto trading platform.”

None of this would matter much, but Russell is an example of an influencer in today’s markets: 160,000 YouTube subscribers, and 100,000 Twitter followers. We can think of him as a useful indicator of sentiment among the new wave of ZIRP investors.

And that sentiment remains strong: recent events are seen as merely a bump in the road to ever greater crypto and tech riches.

The bottom line from me is: I will be happy to declare that asset prices are cheap only when “crypto bros” and their fellow travellers have jumped ship and blamed the Fed, the ECB, the SEC, the CIA, Russia, monkeypox or Bill Gates for the large black craters where their portfolios used to be.

Because that is ultimately what is going to happen.

Until then, while the widespread belief in easy profits from investing in junk assets persists, it’s clear to me that we are very far from the bottom.